Solar PV system costs in the U.S. are falling faster than expected across all market segments, Wood Mackenzie research finds

Solar PV system costs in the US are falling faster than anticipated across all market segments, primarily driven by module price reduction, according to new research from Wood Mackenzie.

The U.S. Solar PV System Pricing, H1 2020 biannual report, which includes detailed breakdowns for system prices in 2020, with forecasts through 2025, finds that residential system prices with mono PERC modules are now expected to fall 17% from 2020 to 2025, up from 14% forecast pre-coronavirus. Additionally, mono PERC commercial and utility system costs are expected to decline 16% and 20%, up from 13% and 16%, respectively, during the same timeframe.

Molly Cox, Wood Mackenzie Research Analyst said:

“In the utility segment, bifacial modules are gaining traction, especially as these modules have been exempt from Section 201 tariffs on all imports into the US.

“Typically, utility-scale bifacial tracker projects would be more expensive than those with monofacial mono PERC modules due to increased interrow spacing, resulting in higher civil and land costs. However, bifacial systems also yield system cost benefits. These include reduced balance of system components and lower labor costs because of the comparatively fewer modules needed when compared to a monofacial system of the same capacity.

“In 2020, while bifacial modules are currently exempt from Section 201 tariffs, bifacial system costs are expected to sit at around 1% less than monofacial mono PERC systems.

“However, in a scenario where bifacial modules were subject to Section 201 tariffs, system costs would be higher than monofacial mono PERC systems.”

As module prices represent a shrinking portion of total system prices, Wood Mackenzie expects a heightened focus on soft cost reduction from EPCs and developers.

Soft costs, such as customer acquisition in the residential market, have been a huge barrier to declining system prices, along with permitting and inspection costs.

However, as hardware costs are expected to decline at a slower pace over the next decade, it will be crucial to understand where the next level of system cost reduction will occur.

“There are efforts under way to address high permitting and inspection costs for residential PV systems. The Solar Foundation and NREL have collaborated to form The Solar Automated Permit Processing platform (SolarAPP), which could yield savings for residential PV systems,” added Cox.

Coronavirus impacts will affect residential system prices more so than any other market segment in 2020, says Wood Mackenzie.

“Residential projects have more exposure to the impact of the coronavirus due to their shorter project cycles.

“While there is near term risk for price increases for larger C&I and utility scale projects, overall 2020 system costs are not expected to be significantly impacted by the coronavirus in these segments.

“Module cost reduction will be the most significant factor impacting C&I and utility system costs as a result of the pandemic. Not only are module manufacturers facing reduced demand and subsequently lowering margins to stay competitive, but they are also looking at a reduction in supply chain component costs, leading to further module price declines,” said Cox.

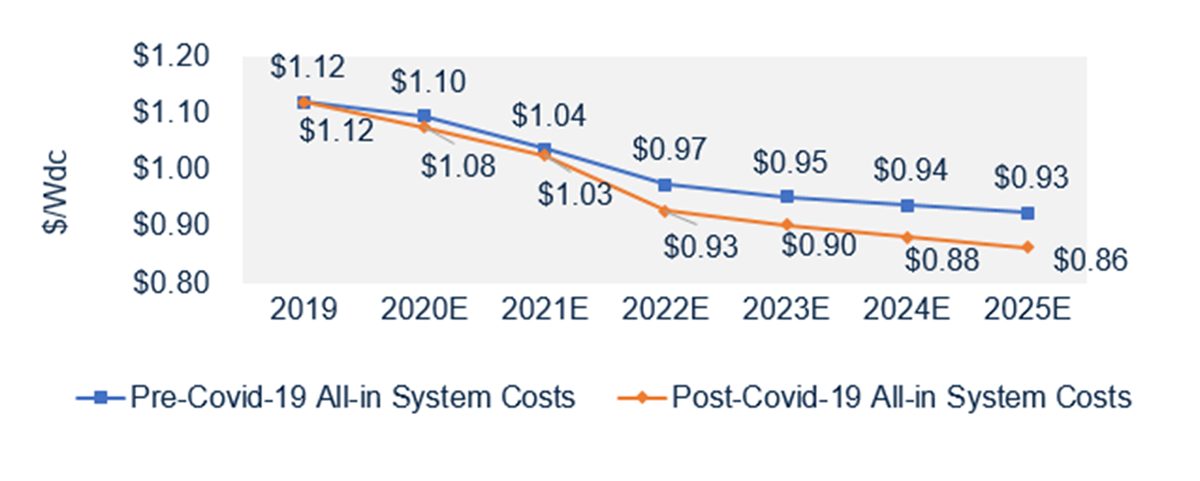

US utility tracker 10 MW PV system costs, pre- and post- Covid-19, 2019 – 2025E

The Investment Tax Credit (ITC) reduction to 26% in 2020 will create further downward price pressure across all market segments, for both EPCs and developers, according to the Wood Mackenzie report.

“The stepdown will cause companies to closely analyze their cost stacks and ensure solar PV systems are still competitive with a 4% ITC reduction. Having said that, companies have been preparing for the ITC stepdown, so we do not expect any drastic changes to system prices in 2020 as a result.

“As the solar industry faces demand destruction in 2020 from coronavirus impact, we expect demand to pick back up again by the end of the year and before the ITC steps down again in 2021.

“As a result, companies across all market segments may be able to maintain healthier project margins towards the end of 2020 as a result of the heightened demand, just like we saw at the end of 2019,” said Cox.

Source: Press Release by Wood Mackenzie.