Total installed solar PV capacity exceeded 500 GW globally in 2018, IEA PVPS report finds

The International Energy Agency Photovoltaic Power System Programme (IEA PVPS) announced the publication of the 7th edition of its report “Snapshot of Global Photovoltaic Markets” on Monday, 15 April 2019.

This report provides estimated data about photovoltaic (PV) capacity in the countries reporting to the IEA PVPS Programme and additional key markets and it serves as a preliminary assessment prior to the 24th edition of the PVPS flagship report “Trends in PV Applications” that will be published at the end of the year.

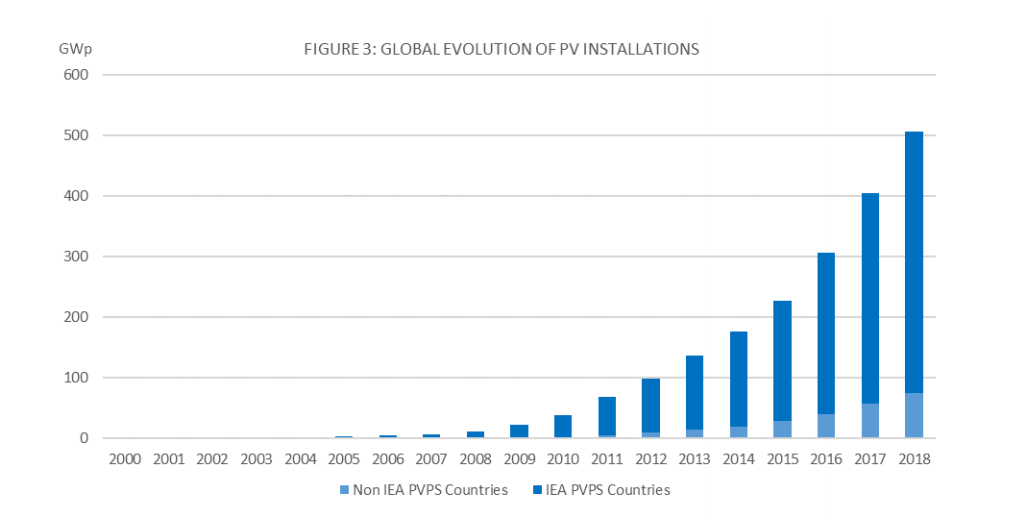

The report states that preliminary market numbers show that the PV market probably stabilized in 2018. In total, about 97,9 GW of PV capacity were installed in the IEA PVPS countries and in other major markets during 2018, and up to 99,8 GW in total (compared to 98,9 GW in 2017). The total installed capacity in the IEA PVPS countries and key markets has crossed the 500 GW mark in 2018, or half a TW.

While the Chinese PV market experienced a limited decline in 2018 to 45 GW, it was compensated with larger installation volumes in several emerging and established markets. Amongst the growing markets, India can be cited, with 10,8 GW, Australia, that increased spectacularly in 2018, with close to 3,8 GW, Mexico follows with close to 2,7 GW, then Korea with 2,0 GW, followed by a declining Turkish market, above 1,6 GW.

The Middle East and African markets experienced growth as well, however a large part of this will be visible in 2019 when most plants will be commissioned, especially in the UAE and Egypt. In the meantime, the US and Japanese market where roughly stable, while Europe grew. The European market rebirth was mainly driven by the significant growth in Germany and the Netherlands, while growth was visible in many countries.

In summary, the global PV market outside of China grew by 9 GW to 55 GW while the decline in China drove the global numbers up to at least 99,8 GW. This growth outside of China composes a different landscape for the PV market, with a 20% growth outside of China.

In total, PV contribution amounts to close to 2,6% of the electricity demand in the world. In the coming years, PV has the potential to become a major source of electricity at an extremely rapid pace in several countries all over the world. The speed of its development stems from its unique ability to cover most market segments; from the very small individual systems for rural electrification to utility-size power plants (today way over 1 GWp).

From the built environment to large ground-mounted installations, PV finds its way, depending on various criteria that makes it suitable for most environments. In 2018, PV was the first electricity source in capacity deployed globally. It follows a rapid growth path, which might be supported in the coming years by two key enablers: the decrease of battery prices and the rapid uptake of electric vehicles.

Highlights

- The total installed capacity for PV crossed the 500 GW mark in 2018, or half a TW.

- The global annual PV market was at least 97,9 GW in 2018. With non-IEA PVPS reporting countries, this number could grow up to 99,9 GW, compared to 76,4 GW in 2016 and 98,9 GW in 2017. The 2,0 GW difference comprises non-IEA PVPS markets countries such as most unreported African, Asian and Latin American countries.

- This year saw the Chinese PV market contracting, from 53,0 to 45,0 GW. China is the leader in terms of total capacity with 176,1 GW installed.

- Outside of China, the global PV market grew from 48,6 GW to 54,9 GW.

- India progressed significantly, as the annual market grew to 10,8 GW, becoming the second-largest PV market, including around 2 GW of distributed and off-grid installations.

- The US market decreased slightly to 10,6 GW, with utility-scale installations accounting for roughly 60% of additions.

- The European Union installed 8,3 GW and the rest of Europe added roughly 1,1 GW. The largest European market in 2018 was Germany (3,0 GW), followed by the Netherlands (1,3 GW), and France (862 MW).

- Japan ranks fourth, with around 6,5 GW annual installed capacity.

- Other markets increased spectacularly in 2018, especially Australia, with close to 3,8 GW, Mexico with close to 2,7 GW, Korea with 2,0 GW, followed by a declining Turkish market, still above 1,6 GW.

- The MEA markets experienced growth, but a large part of this will be visible in 2019 when most plants will be commissioned, especially in the UAE and Egypt.

- In the top 10 countries, there are now five Asia-Pacific countries (China, India, Japan, Australia and Korea), two European Union countries (Germany and the Netherlands) plus Turkey, and two countries in the Americas (the USA and Mexico).

- The level to enter the top 10 markets in the world in 2018 was around 1,6 GW, the highest level ever and the first time significantly above the GW mark.

- The top 10 countries represented 87% of the global annual PV market.

- Honduras, Chile, Germany, Greece, Italy, Japan, Australia, India and Morocco now have enough PV capacity to theoretically produce more than 5% of their annual electricity demand with PV.

- PV represents around 2,6 % of the global electricity demand and 4,3 % in Europe.

32 countries had at least 1 GW of cumulative PV systems capacity at the end of 2018 and 10 countries installed at least 1 GW in 2018.

[embeddoc url=”http://solarbusinesshub.com/wp-content/uploads/2019/04/IEA-PVPS_T1_35_Snapshot2019-Infographic.pdf” download=”all”]

Source: Press Release by IEA PVPS.